| X.ts <- ts(X, frequency=12, start=c(2010,1)) | | #1: store the data in a time series object |

| X.diff <- diff(X.ts, differences=1) | | #2: assuming not stationary then we need differencing |

| par(mfrow = c(3,1)) | | #3: 3x1 charts |

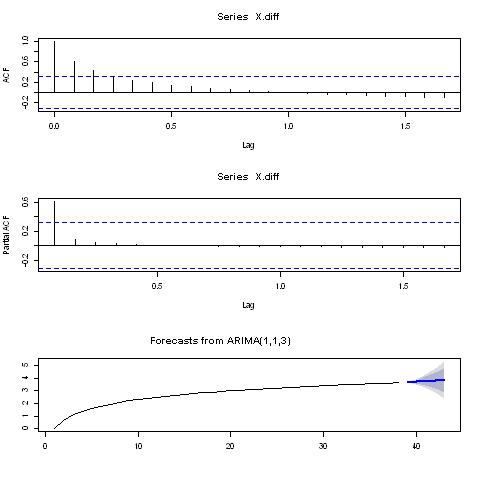

| acf(X.diff, lag.max=20) | | #4: correlogram for lags 1-20 to find q |

| pacf(X.diff, lag.max=20) | | #5: partial correlogram for lags 1-20 to find p |

| library("forecast") | | #6: load the "forecast" R package |

| #X.arima <- auto.arima(X) | | #7: find an appropriate ARIMA model |

| X.arima <- arima(X, order=c(1,1,3)) | | #7: use ARIMA(p,d,q) where p=1,d=1,q=3 |

| X.arima | | #8: display ARIMA model |

| X.forecasts <- forecast.Arima(X.arima, h=5) | | #9: forecast up to the next 5 period |

| plot.forecast(X.forecasts) | | #10: plot forecast |